Lack of Inventory Causing Headache for Buyers in Westside/South Bay Markets

Usually when one picks up the LA Times and reads about a fledgling housing market or tunes to the business networks on TV and sees signs of national distress, they naturally believe a buyer in this market would have all of the leverage. Unfortunately for buyers searching for phenomenal deals on the Westside and Manhattan Beach deals are extremely hard to come by thanks to a severe lack of inventory.

Westside prices which in our estimation are higher than they should in the grand scheme of things have stabilized and even gone up in some areas this year. Our recent Townhouse listing at 2922 Montana Ave. Unit B recently sold in three weeks for $1.1M, 70K higher than a similar unit in the building sold four months prior. Though we would love to take all of the credit for the uptick as the agent (will take some along with the stellar job of staging by our client), the reality is we were helped by the fact that we did not have much competition for a stylish unit in a great location.

Westside prices which in our estimation are higher than they should in the grand scheme of things have stabilized and even gone up in some areas this year. Our recent Townhouse listing at 2922 Montana Ave. Unit B recently sold in three weeks for $1.1M, 70K higher than a similar unit in the building sold four months prior. Though we would love to take all of the credit for the uptick as the agent (will take some along with the stellar job of staging by our client), the reality is we were helped by the fact that we did not have much competition for a stylish unit in a great location.

In the 90402 zip there are only 15 new listings since March 1st. Of those, 3 are already in escrow. Areas like Mar Vista have seen 30% of new listings sell within 20 days of coming on the market and we can give you individual examples of clients recently losing out in multiple offer situations to bids that appeared to be above market. Multiple offer situations have been feverishly popping up in all price ranges as long as the property is priced at market.

This has been frustrating many buyers who have recently moved to the area or have been waiting for an opportunity to buy prime real estate. It doesn’t make logical sense in comparison to the economy as a whole and here are the reasons as to why this is happening.

Massive amount of purchases during the bubble peak: Most high priced areas like the Westside and Manhattan Beach saw historical sales volume between 2004 and 2007, at or near the top of the peak. Many of these purchases were done with less than 20% down (many at 5-10% even in the jumbo markets) and buyers were turning around and refinancing if prices trended upward after they bought. These purchasers now owe quite a bit more than the home is worth and are simply not in position where they can afford to sell. They also refinanced at historically low rates and if they are in a similar position from a job standpoint they are simply stuck and “hanging on” until a significant jump in the market happens. Short sales and foreclosures are happening but only with people in dire financial straits and many on the Westside tend to have jobs or family money to help them. Speaking of foreclosures and short sales…

Shadow inventory has not appeared: Bank owned homes and short sales have been slow to hit prominent markets like the Westside. Banks are incentivized to slowly release high priced assets. Until they lose a loan valued at $2.5M, the banks can report it as an asset at that value even though it may only be worth $1.8M. Once that asset sells for $1.8M, the bank not only loses a $2.5M asset but also reports a loss of $700K. Legislation slowing down foreclosures in California has also hurt this pipeline. I am currently working on one short sale where the seller has been in default for over 15 months and we have yet to reach an auction date. The short sale process has also contributed to this mess with some taking over a year to close from beginning to end. Expect the shadow inventory to continue to hit the market at a snail’s pace.

Buyers are anxious: Due to the lack of opportunity for purchasers cited above the leverage they enjoyed in 2009 and the first part of 2010 is dissipating for now. Many purchasers have been waiting for the right opportunity to buy on the Westside and feel now is the time with interest rates at or near record lows with the looming threat of rates going higher as the economy seems to recover.

When you couple this mentality with a strong pool of international buyers (most notably all cash buyers China and Europe taking advantage of the weak dollar) and tech companies like Google and Facebook strategically opening offices on the Westside, you end up with a strong pool of purchasers competing for a limited product causing quite a bit of frustration.

Another factor pushing buyers valued in the $800K-$1M range is the conforming loan rate of $729,500 is expiring October 1st and being replaced by a rate limit of only $625,000. Loans above $625K will be a a higher rate and that $100K+ difference will definitely impact the market and what one can afford to buy.

For now, purchasers have to understand what they are dealing with due to the circumstances above. The days of trying to “steal” a property have been suspended for the time being and replaced with patience and knowing they are not the only ones out there. It is a good time for a seller to list a home and get good terms from a buyer if they are willing to acknowledge about a 20% cut from bubble prices.

1st Quarter Sales trends compare favorably to 2010 in Manhattan Beach

*Note on graph: WoS only stands for West of Sepulveda

*Note on graph: WoS only stands for West of Sepulveda

There were more closed sales in the first quarter of 2011 than in any year since 2007,when the bubble was starting to super inflate and get ready to pop, which is extremely apparent when examining the above graphic.

The boost in sales was +9 for Manhattan Beach as a whole and when you look at the micro market West of Sepulveda. Though sales increased, the median price of sales West of Sepulveda dropped 7% from $1.607M in the first quarter of last year to $1.50M this year.

Overall, the whole city of Manhattan Beach saw an increase in sale price from $1.430M in the 1st quarter of 2010 to $1.5M this year. Though prices declined West of Sepulveda, the increase in overall price is directly related in the increase in sales in the higher priced area.

Please note that tracking sales on a quarterly basis can skew the numbers especially when sales volume is relatively low. For example, the 4th quarter of 2010 median price was $1.362M west of Sepulveda, and $1.252M for all of MB. If you were to compare the most recent quarters to quarters, you would think Manhattan Beach prices went up 20% at the snap of a finger. Obviously that is not the case.

Another interesting and important thing to look at is how the % of Single Family Residences selling above $1M has changed dramatically since 2008 when the bubble started to officially burst.

In the first quarter of 2006, just 6% of all homes sold in Manhattan Beach sold for less than $1M. This year 27% of homes sold for less than $1M, statistically, that is a 450% increase in homes selling below $1M.

In terms of sales above $2M, during the late-boom year of 2006, almost half the homes sold in Q1 went for $2M oe more (44%). The median price that quarter was $1,972,500.

This year 83% of the homes sold in Manhattan Beach in Q1 sold for less than $2M.

Manhattan Beach West of Sepulveda fared about the same over this 6-year period. Sales above $2M were 22% of the sales in the first part of 2011, down from 48% in 2006. Sales above $2M are at a six year low.

(*Source: Manhattan Beach Confidential – article and graph)

Articles You Should Read

1- So Cal rents are likely to remain flat according to USC study: The steep declines in rent that were seen the past few years are beginning to ebb and places to rent on the Westside are becoming difficult to find. We believe renters on the Westside and in areas like Manhattan Beach should expect a 1-3% increase over the next 12 months. Here is an article about the broad So Cal rental market from the LA Times: Southern California rents are likely to remain flat, study says

2- Changes in mortgage finance rules will hurt housing recovery: Some of the requirements that federal agencies and the Obama administration are proposing will prove troublesome for consumers as you would need to spend no more than 28% of your gross monthly income on housing-related expenses, and you couldn’t have total monthly household debt that exceeds 36% of your income. There would be not flexibility beyond these ceilings. This is just one of the myriad of changes proposed that you can read about in this article from the LA Times.

3- Experienced appraisers getting priced out by banks: Accurate appraisals are extremely important in the current market and can be deal breakers when inexperienced appraisers get assigned to areas they do not know how to valuate. Lenders are not paying experienced appraisers enough ($200-$250) to cover their overhead costs yet they are charging the consumer $450. Less-experienced appraisers who sometimes have to travel long distances from their home markets tend to be more willing to work for the lower amounts and can create nightmare scenarios for transactions on the Westside and Manhattan Beach where the sale price can change 150-300K one street over. LA Times article: Are you getting your money’s worth with appraisal?

New Legislation Would Make Short Sale Process Quicker

Legislation proposed last week in the House of Representatives would make short sales faster.

The bill, with bipartisan backing would require banks and mortgage servicers to respond to requests for a short sale within 45 days of the request. This would be great news as getting negotiators on short sales to call back in this time frame is a nightmare even with daily phone calls to them.

A short sale is when a bank allows a borrower with negative equity to sell their home for less than is owed on the mortgage. The difference between the sale price and what is owed on the mortgage is usually then forgiven by the lender. They are most common in markets such as California where home prices have declined dramatically since the market peaked.

The problem is that in the era of mortgage securitization, multiple parties (investors, servicers, insurers, etc.) need to acquiesce to a short sale in order to complete the deal.

It can take an extremely long time for all involved parties to get back to the buyer and seller with an answer. It was recently found that in California, 4 out of 10 short sales that go under contract end up falling through. This is a direct result of the lengthy short sale process.

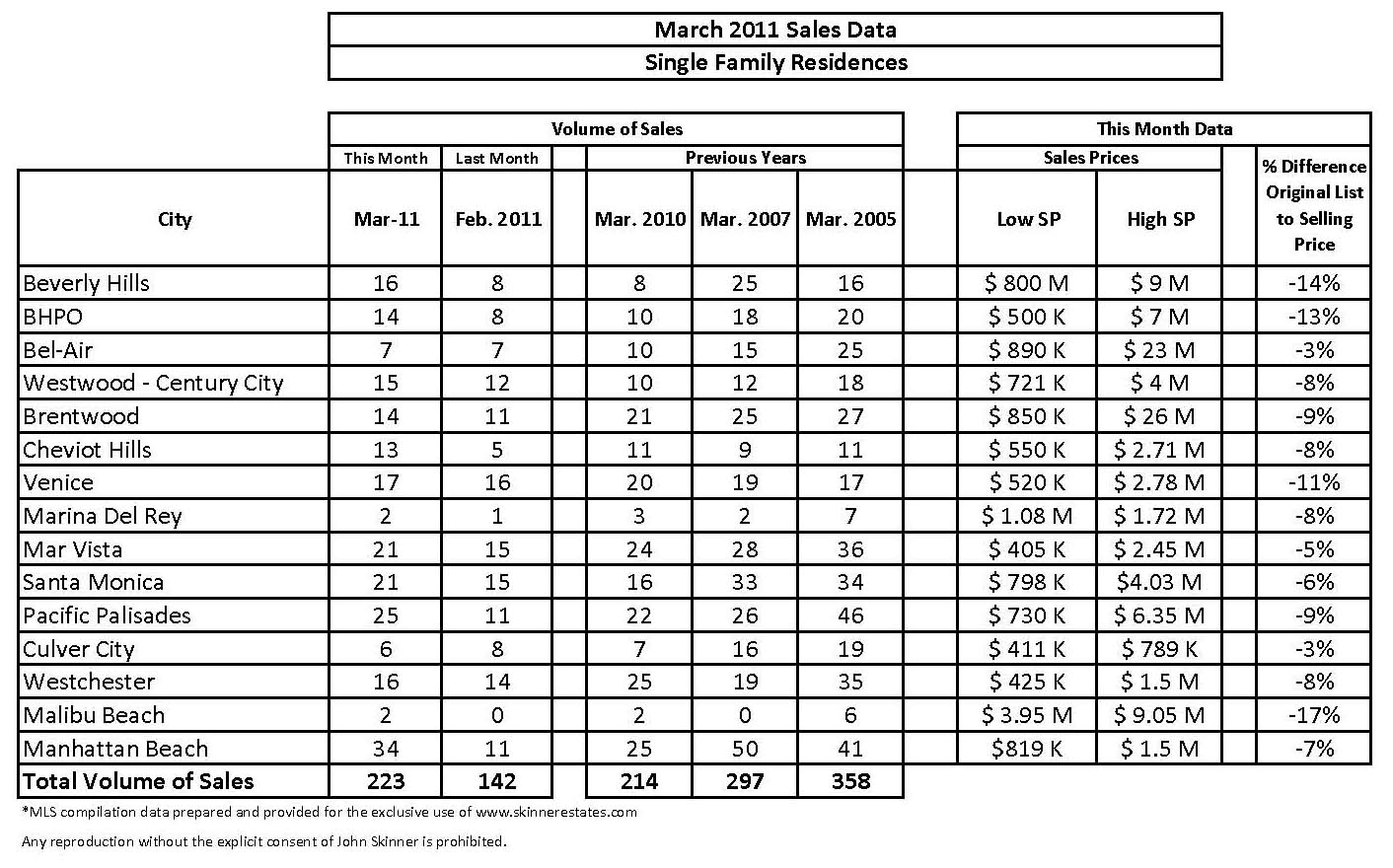

In-Depth Look at Single Family Sales in March for the Westside/Manhattan Beach

Sales volume increased 57% in March compared to February but only increased 4.2% over last March and down 33% and 60% when compared with the Wild West days of 2007 and 2005.

Sales volume increased 57% in March compared to February but only increased 4.2% over last March and down 33% and 60% when compared with the Wild West days of 2007 and 2005.

The difference between the average original list price and sales price also improved dramatically compared to February. With the exception of February, the recent trend shows Seller’s are being more realistic with their initial sales price and due to a lack of inventory we are seeing quite few multiple offer situations. Like the condo market, the buyer still has the leverage but it is not nearly as lopsided as previous years.

Every area saw an increase in sales except Culver City and Bel-Air.

Manhattan Beach increased in sales 4x’s with 34 in March compared to 11 in February. Most of these sales were on the lower end for Manhattan Beach. This past March was also 36% better than March 2010. They still fall short of the robust 50 sales in March of 2007 but definitely showing signs of life especially with first time homebuyers itching to enjoy that unparalleled Manhattan Beach lifestyle.

Beverly Hills Post Office popped with 14 sales, almost doubling last month’s output and beating March 2010 by about 40%. Sales ranged from $500k to 7M.

A look at a few individual sales that stood out:

12218 Octagon St- Brentwood: This North of Sunset home in need of major remodeling sold 10% above the original list price at $1.302M. It sold in 7 days and is a 3+2, 1,688 sq. ft. on a 9,583 sq. ft. lot. The low list price created an auction like atmosphere with multiple all cash buyers vying for the property.

12218 Octagon St- Brentwood: This North of Sunset home in need of major remodeling sold 10% above the original list price at $1.302M. It sold in 7 days and is a 3+2, 1,688 sq. ft. on a 9,583 sq. ft. lot. The low list price created an auction like atmosphere with multiple all cash buyers vying for the property.

11930 Currituck Dr- Brentwood: In between Montana and Sunset, this woodsy 2+1.75, 1,218 sq. ft. home on a 5,488 sq. ft. lot sold for $1.01M, 26% below its original list price! However, most would make you believe it sold for over asking with a last list price of $999K. This could may have been a short sale as it was bought in 2005 for $1,275,000.

2425 Frey Ave- Venice: Bank owned sale ends up going for 31% below ($895K) the original list price of $1.3M. This contemporary and recently updated 3+2, 2,640 sq. ft. home ended up being a terrific buy.

2425 Frey Ave- Venice: Bank owned sale ends up going for 31% below ($895K) the original list price of $1.3M. This contemporary and recently updated 3+2, 2,640 sq. ft. home ended up being a terrific buy.

746 26th street- Santa Monica– This frantic auction brought out the builders looking for a deal. Despite being on a busy street, the 8,700 sq. ft. lot is coveted and the “auction” list price of $799K brought buyers in by the droves. It ended up selling for $1.1M, 38% above asking. . .

616 25th Street- Santa Monica– Lot values North of Montana still trending lower. In our estimation, this tear down approximately sold for $1.684M even though they only reported a $1 sale price (shame on them). The most important info…8,700 sq. lot near Franklin Schol…

616 25th Street- Santa Monica– Lot values North of Montana still trending lower. In our estimation, this tear down approximately sold for $1.684M even though they only reported a $1 sale price (shame on them). The most important info…8,700 sq. lot near Franklin Schol…

7049 Birdview- Malibu– After being on the market for close to three years, 7049 Birdview finally sold for $9.045M, less than half its original asking price in 2008 of $19,950,000. How the mighty have fallen. This 6,397 sq. ft. home sits on an acre of land and boasts endless coastline and ocean views…

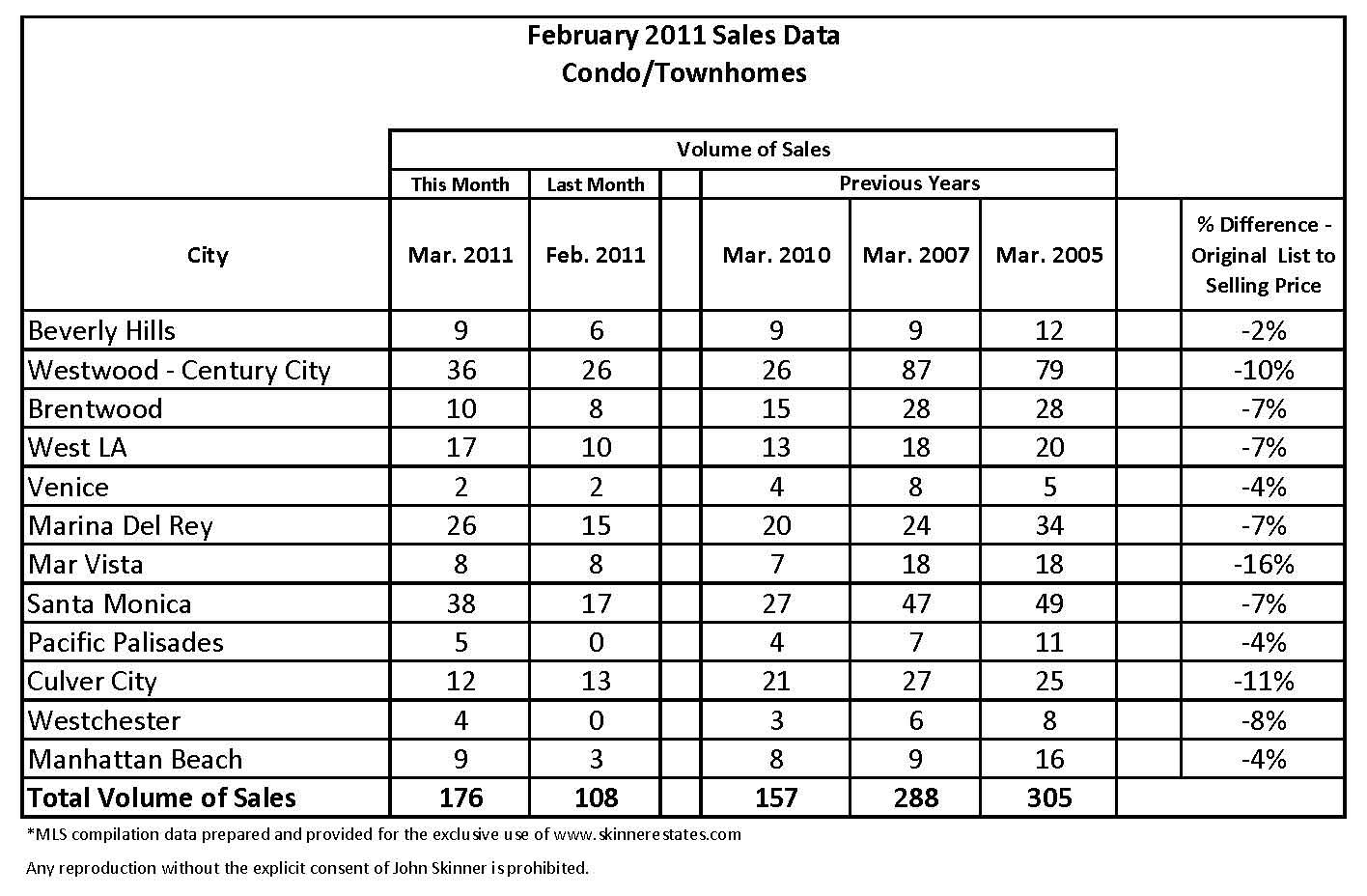

In-Depth Look at Condo/Townhouse Sales in March for the Westside and Manhattan Beach

Overall, we saw a solid increase in sales volume over February, which was expected. However, the increase in sales of 62% over last month was unexpected and the 12% growth in sales over March 2010 continues to show the market is growing steadily out of the Great Recession. Though the numbers look good, we are still off nearly 63% from sales volume 2007 and 73% from the Wild West days of 2005.

In looking at particular areas, Santa Monica had a great month of sales with 38 compared to a dismal February of 17. Santa Monica is up 40% in sales volume compared to March 2010. Most of the seller’s did a good job of pricing the property with the difference in Original List Price to Sale Price at -7% and the difference in List Price to Sale price being around -5%.

Marina Del Rey had a phenomenal month with increasing sales over February by 73% and having a better month than March 2007 which is very rare. Some of this can be attributed to quite a few short sales going through in some of the mid 2005 constructed towers that were flooded with liar loans.

Both Santa Monica and Marina Del Rey are being aided by an influx of buyers thanks to the multitude of tech companies opening offices in the area. It is still considered a buyer’s market but the leverage buyer’s have enjoyed over the past few years is receding somewhat. The good news for sellers is that if they price the unit at or around market value they should be able to sell quickly with good terms.

A look at a few individual sales in Santa Monica:

914 14th Street #101- Built in 2008 along with 4 other units, this 2+2.5, 1,580 sq. ft. unit sold for above asking at $1.150M and was on the market for just 11 days. The asking price was $1.125M. This is the fourth unit to sell in the building with two others selling in 2010 for $687 and $677 per sq. ft. This was the front unit and it sold for $727.85 a square foot. This unit debut on the market for $1.299M in 2008 before being rented out.

914 14th Street #101- Built in 2008 along with 4 other units, this 2+2.5, 1,580 sq. ft. unit sold for above asking at $1.150M and was on the market for just 11 days. The asking price was $1.125M. This is the fourth unit to sell in the building with two others selling in 2010 for $687 and $677 per sq. ft. This was the front unit and it sold for $727.85 a square foot. This unit debut on the market for $1.299M in 2008 before being rented out.

1033 Ocean Ave.#401- After being on the market for 304 days, this luxurious 2+2, 1,396 sq. ft. unit with amazing ocean views finally sold for $1.550M. It was originally listed at $1.850M and went for $1,110 per sq. ft.

Little Change in Mortgage Rates

The average mortgage rates available to borrowers with good credit and 20% down payments or home equity rose a notch.

Freddie Mac said the typical rate for a 30-year fixed loan was 4.87% this week, up from 4.86% last week. The average offering rate for 15-year fixed mortgages was 4.10% compared to 4.09% a week ago.

The lenders were requiring well-qualified borrowers to pay an average of 0.7% of the loan amount in “points” to obtain those rates. Additional third-party charges such as appraisal and title insurance fees are also often added to borrowers’ upfront costs.

Jumbo loans have been running about six-tenths of a percentage point higher than Freddie and Fannie loans in private surveys of the market.

The limit for Freddie and Fannie loans in high-cost areas such as Los Angeles and Orange counties is scheduled to drop on Oct. 1 to $625,500 from the current level of $729,750.

Variable loans with a fixed rate for the first five years were starting at an average 3.72% and 0.6 points, compared to 3.70% a week earlier.

*Source: LA Times

Another tech giant moves to the Westside

With Google creating an office campus in Venice, Facebook has now signed a lease to occupy anywhere between 8,000 and 15,000 square feet in Playa Vista. Over the past year, Venice, Santa Monica and Playa Vista have become quite popular destinations for these Silicon Valley companies and it is great news for our local real estate market and helps partially explain the influx of buyers we have seen.

Here is an article from the Los Angeles Business Journal: Another Tech Giant Moves to the Westside

Proposal would force banks to allow short sales for delinquent homeowners

Major banks may be forced to let severely delinquent homeowners sell their houses for less than the loan amounts owed as part of a broad settlement of federal and state investigations into botched foreclosure paperwork, according to government officials involved in the negotiations.

The requirement to allow so-called short sales would be in addition to forcing mortgage servicers to reduce the amount some homeowners owe on their loans, said two officials, who spoke on the condition of anonymity because negotiations are ongoing.

In Southern California, short sales made up an estimated 19.8% of the market for previously owned homes last month.

Though struggling homeowners escape weighty mortgage debts quickly under a short sale, they don’t get away unscathed.

Their credit scores are damaged enough to limit their borrowing capability for years, though the damage is perhaps less severe than in foreclosure. Money for down payments and renovations would be lost, and there may be tax consequences.

The California Assn. of Realtors has been pushing for short sales to be made simpler. Earlier this month, in an open letter in the Los Angeles Times and six other California newspapers, the group called on banks to approve more short sales and for regulators to streamline the process.

For the complete LA Times article: Proposal would force banks to allow short sales